Ford’s partnership with Amazon enables customers to shop certified used Ford vehicles online through a streamlined, transparent buying process. By integrating dealer inventory with Amazon’s platform, shoppers gain faster comparisons, clear pricing, and a convenient digital path to purchasing their next used car.

KumDi.com

Ford partners with Amazon to reshape the online used-car buying experience by bringing dealer-certified Ford vehicles directly onto one of the world’s largest e-commerce platforms. This collaboration offers buyers a faster, clearer, and more modern way to explore, compare, and secure a quality used vehicle from trusted Ford dealers.

Table of Contents

A Strategic move to meet consumers where they already shop

Consumers increasingly expect to handle large portions of their purchase journey online, from ordering groceries to buying electronics and home furniture. It was only a matter of time before automotive retail followed suit. Ford’s decision to list certified pre-owned vehicles on Amazon aligns perfectly with the changing expectations of today’s digitally empowered shoppers.

By positioning used vehicles within Amazon’s ecosystem, Ford taps into a platform that millions of Americans visit daily. Buyers who already trust Amazon’s buying processes can now apply that familiarity to one of the most significant purchases in their lives—a car. For Ford, this partnership is a way to reach customers early in their search journey and offer a modern, transparent buying experience that reduces friction.

More importantly, this move strengthens Ford’s broader strategy of blending digital convenience with traditional dealership benefits. Instead of replacing dealers, Ford is enhancing their reach by giving them access to an enormous online audience.

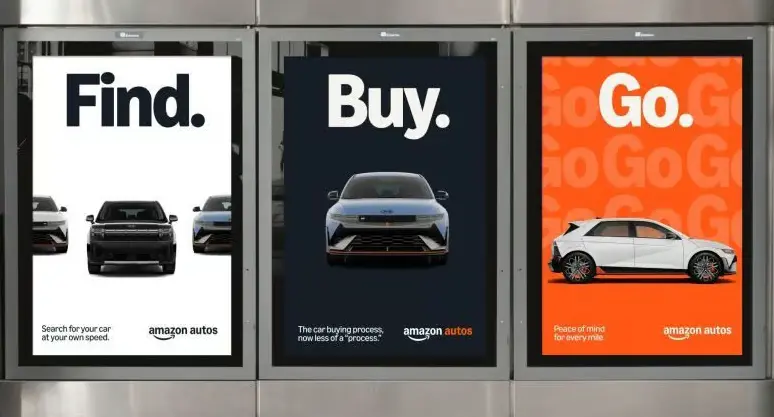

How the Amazon used-vehicle buying experience works

Ford’s new online experience is designed to be intuitive, straightforward, and aligned with how people already navigate Amazon.

1. Browse certified pre-owned vehicles

Customers can explore Ford’s certified used inventory directly within Amazon’s Autos category. Listings include detailed images, reconditioning notes, mileage information, warranty specifics, and inspection results. Buyers can filter by model, trim, year, budget, and location, making it easier to find a vehicle that meets their exact needs.

2. Complete much of the purchase online

The process offers an online-first workflow that dramatically streamlines the steps traditionally done in person. Customers can complete paperwork, explore financing, estimate monthly payments, review trade-in options, and confirm key purchase details—all from home. This reduces uncertainty and eliminates wasted time at a dealership.

3. Arrange pickup at a participating Ford dealer

Instead of having cars shipped or delivered, buyers pick up their vehicle at the selling dealership. This ensures the dealer remains a crucial part of the transaction while also giving customers peace of mind through a final in-person review of the car. Buyers can also schedule optional test drives before finalizing paperwork.

4. Certified quality through Ford’s verification program

All vehicles listed through this program are certified through Ford’s own inspection and reconditioning processes. This gives buyers added confidence compared to purchasing through third-party used-car platforms, where inspection standards can vary significantly.

Why Ford chose Amazon—key motivations behind the partnership

Ford’s collaboration with Amazon wasn’t simply about expanding online visibility. It reflects deeper strategic goals shaped by evolving market conditions, new competitors, and shifting consumer behavior.

1. Modernizing the used-car buying journey

Consumers have grown accustomed to convenience and clarity in their online shopping experiences. Ford’s goal is to replicate the simplicity of ordering a product on Amazon—clear pricing, easy navigation, and predictable steps—within the more complex world of automotive retail.

2. Enhancing the role of Ford dealers

Rather than bypassing dealers, Ford designed this initiative to empower them. Selling used vehicles on Amazon gives dealerships a new avenue to showcase their certified inventory and attract customers they might otherwise never reach.

3. Competing in a rapidly expanding digital-first used-car market

The rise of online-only auto retailers has reshaped the landscape. Ford’s presence on Amazon allows it to remain competitive against digital-native brands by offering both the convenience of online shopping and the reassurance of its nationwide dealer network.

4. Leveraging Amazon’s massive customer base and trust factor

Amazon has become a trusted environment for making significant purchases. Listing vehicles on this platform taps into that trust and gives Ford access to millions of buyers who may not have considered visiting a dealership in person.

Benefits for customers: A smoother, more transparent way to buy used cars

From a consumer perspective, Ford’s move brings several major advantages:

1. Increased transparency

Detailed listings, certified inspection results, and upfront pricing help eliminate the guesswork that often comes with used-car shopping.

2. Less time spent at dealerships

Much of the process is completed online, reducing dealership time to pickup and final confirmation, rather than hours of negotiation.

3. Familiar shopping environment

The Amazon interface is intuitive and trusted, lowering the psychological hurdles of making a large purchase online.

4. Certified vehicles only

Customers get peace of mind knowing each vehicle has undergone Ford’s quality and safety checks.

5. Better comparison shopping

Shoppers can quickly compare models, trims, and prices without driving from lot to lot.

How Ford dealers benefit from the Amazon partnership

Dealerships remain at the heart of this initiative. The partnership isn’t about replacing dealer operations—it’s about modernizing them.

1. Greater online visibility

Dealers gain exposure on one of the world’s largest digital platforms, reaching buyers beyond their local region.

2. Streamlined customer interactions

By the time a customer arrives to pick up a car, much of the work is already done. This improves efficiency and reduces time spent on administrative tasks.

3. Increased foot traffic for future sales and service

Even customers picking up used cars may return for maintenance, repairs, or future purchases.

4. Differentiation from competing dealerships

Dealers participating in the Amazon program may gain an edge over those who still rely entirely on traditional marketing.

Impact on the broader automotive market

Ford’s partnership with Amazon could reshape the used-car market across several dimensions:

1. Accelerating the digital transformation of car buying

Consumers will increasingly expect the ability to complete more of the vehicle purchase process online.

2. Setting a precedent for other automakers

Other major brands may follow Ford’s lead and pursue partnerships with major digital marketplaces to strengthen their used-car strategies.

3. Reducing friction in one of the most stressful consumer transactions

Purchasing a vehicle is often considered stressful. Ford’s new approach aims to simplify the journey, which may reset industry expectations over time.

4. Blending e-commerce with dealership reliability

This hybrid model—online browsing with local pickup—could become the new standard for used-car retail.

A significant milestone in automotive e-commerce

Ford’s partnership with Amazon is more than a convenience upgrade—it’s a signal of where the industry is heading. By giving dealers the tools to sell certified used vehicles in a modern online environment, Ford is embracing the future while preserving the value of its long-established dealership network.

Buyers gain transparency, speed, and a familiar purchasing experience. Dealers gain increased visibility and more efficient operations. And Ford positions itself at the forefront of digital automotive retail, laying the foundation for future innovations in both new and used vehicle sales.

As the automotive world continues to shift toward online experiences, Ford’s collaboration with Amazon may well become a blueprint for the industry—a seamless blend of digital convenience and trusted local service.

FAQs

What does it mean that Ford partners with Amazon for online used-car buying?

Ford partners with Amazon to list dealer-certified used vehicles on Amazon’s platform, allowing shoppers to browse, compare, and begin their purchase online. This makes online used-car buying faster and connects buyers directly to Ford dealer certified vehicles.

How does the Ford–Amazon online used-car buying process work?

Customers search Amazon’s auto section for dealer certified vehicles, review details, complete steps online, and finalize at a local Ford dealer. This creates a seamless Amazon auto shopping experience with the trust of Ford dealers.

Are the used cars sold on Amazon certified by Ford dealers?

Yes, all vehicles listed through the Ford partners with Amazon program are Ford dealer certified vehicles. This ensures high inspection standards, quality assurance, and a trustworthy online used-car buying experience.

What are the benefits of purchasing a Ford used car on Amazon?

Shoppers gain transparent pricing, detailed listings, and simplified Amazon auto shopping, supported by Ford dealer certified vehicles. The process saves time and offers a familiar, fast digital buying environment.

Can buyers test-drive vehicles purchased through the Ford–Amazon partnership?

Yes. After selecting a vehicle through the Ford partners with Amazon program, customers schedule a pickup or test drive at the Ford dealer. This blends online used-car buying convenience with in-person reassurance at certified dealerships.

{kind=link}